library(tidyverse)

library(estimatr) # Estimation with robust standard error

library(MatchIt) # Matching for preprocess

Data_R <- read_csv("ExampleData/Example.csv")4 線形モデルによるパラメータの推定

関心のあるパラメータ\(\tau(X)=E[Y|d,X]-E[Y|d',X]\)を埋め込んだ線形モデルを推定する。

- 典型的には、\(E[Y|D,X]\)を線形近似し、推定する。

\[E[Y|D=d,X=x]=\underbrace{\tau}_{Interest\ parameter}\times d+\underbrace{f(x)}_{Nuisance\ function}\] - \(f(X)=\beta_0 + \beta_1 X_1 + ...+\beta_LX_L\)

\(\tau\)について点推定だけでなく、信頼区間も推定する。

Section 4.2 線形モデルを推定し、信頼区間を計算する方法を紹介

Section 4.3 近似モデルの定式化への依存度を下げるために、マッチング法を用いた前処理を導入

Section 4.4推定結果の表によるまとめ、可視化、および複数の推定結果を効率的に保存する方法を紹介

4.1 設定

4.2 パラメータの推定

\(\tau(x)=\tau,f(x)=\beta_0+\beta_1x_1+...+\beta_Lx_L\)と特定化

サンプル内MSEを最大化するように推定

線形モデルによる推定は、いくつかの問題がある

異なるグループ間で、\(X\)の分布が異なる場合、回帰式の定式化に強く依存する

一般に平均効果ではなく、加重平均が推計される

サンプルサイズに比べて、少数のコントロール変数を導入できない

以下ではマッチング法、機械学手法を用いた頑強な推定を目指す

robust standard errorを計算するためにestimatrパッケージを利用

lm_robust関数で推定

lm_robust(Price ~ Reform + TradeQ + Size + BuildYear + Distance, # Outcome ~ Treatment + Controls

data = Data_R) Estimate Std. Error t value Pr(>|t|) CI Lower

(Intercept) -1388.4988461 26.32698942 -52.740510 0.000000e+00 -1440.1030211

Reform 3.8725217 0.43467146 8.909078 5.737306e-19 3.0205116

TradeQ 0.6242352 0.19779659 3.155945 1.602999e-03 0.2365293

Size 0.8355270 0.01284035 65.070430 0.000000e+00 0.8103583

BuildYear 0.6981813 0.01307451 53.400209 0.000000e+00 0.6725537

Distance -1.4171745 0.04437330 -31.937548 1.679446e-216 -1.5041516

CI Upper DF

(Intercept) -1336.8946710 14787

Reform 4.7245319 14787

TradeQ 1.0119411 14787

Size 0.8606957 14787

BuildYear 0.7238090 14787

Distance -1.3301973 14787statsmodelsパッケージを利用

heteroscedasticity robust (HC3)を設定

results = smf.ols('Price ~ Reform + TradeQ + Size + BuildYear + Distance', data=Data_Python).fit(cov_type='HC3')

print(results.summary()) OLS Regression Results

==============================================================================

Dep. Variable: Price R-squared: 0.425

Model: OLS Adj. R-squared: 0.425

Method: Least Squares F-statistic: 1197.

Date: Sun, 12 Mar 2023 Prob (F-statistic): 0.00

Time: 14:49:42 Log-Likelihood: -67666.

No. Observations: 14793 AIC: 1.353e+05

Df Residuals: 14787 BIC: 1.354e+05

Df Model: 5

Covariance Type: HC3

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

Intercept -1388.4988 26.334 -52.726 0.000 -1440.113 -1336.885

Reform 3.8725 0.435 8.906 0.000 3.020 4.725

TradeQ 0.6242 0.198 3.155 0.002 0.236 1.012

Size 0.8355 0.013 65.048 0.000 0.810 0.861

BuildYear 0.6982 0.013 53.385 0.000 0.673 0.724

Distance -1.4172 0.044 -31.928 0.000 -1.504 -1.330

==============================================================================

Omnibus: 33924.864 Durbin-Watson: 1.199

Prob(Omnibus): 0.000 Jarque-Bera (JB): 1076517538.013

Skew: 21.520 Prob(JB): 0.00

Kurtosis: 1323.863 Cond. No. 3.28e+05

==============================================================================

Notes:

[1] Standard Errors are heteroscedasticity robust (HC3)

[2] The condition number is large, 3.28e+05. This might indicate that there are

strong multicollinearity or other numerical problems.4.2.1 RCTデータへの応用

原因変数が完全にランダム化されている場合、因果効果の識別を目的に回帰分析を応用する必要はない

因果効果の推定の改善、効率性向上、を目的とした線形モデルの利用は議論されてきた

Lin (2013) は、以下のような交差項を導入したモデルを用いることで、平均の差の推定に比べて、漸近的効率性が悪化することはない(同等か改善する)ことを示した

\[E[Y|D,X]=\beta_{D}\times D+\beta_1\times X_1+...+\beta_L\times X_L\]

\[+\underbrace{\beta_{1D}\times D\times X_1+...+\beta_{LD}\times D\times X_L}_{交差項}\]

- lm_lin関数で推定可能

lm_lin(Price ~ Reform, # Outcome ~ Treatment

~ TradeQ + Size + BuildYear + Distance, # ~ Controls

data = Data_R) Estimate Std. Error t value Pr(>|t|)

(Intercept) 38.574938756 0.23419642 164.7119043 0.000000e+00

Reform 3.198398709 0.46416205 6.8906941 5.776551e-12

TradeQ_c 0.589548934 0.24839614 2.3734223 1.763681e-02

Size_c 0.836196335 0.01462551 57.1738400 0.000000e+00

BuildYear_c 0.742123631 0.01496681 49.5846277 0.000000e+00

Distance_c -1.393206627 0.05322394 -26.1763134 1.120269e-147

Reform:TradeQ_c 0.172655995 0.37815512 0.4565745 6.479836e-01

Reform:Size_c -0.004222054 0.03058905 -0.1380250 8.902225e-01

Reform:BuildYear_c -0.154969457 0.03044214 -5.0906230 3.612720e-07

Reform:Distance_c -0.086574362 0.09590703 -0.9026905 3.667049e-01

CI Lower CI Upper DF

(Intercept) 38.11588462 39.03399290 14783

Reform 2.28858332 4.10821410 14783

TradeQ_c 0.10266158 1.07643629 14783

Size_c 0.80752852 0.86486415 14783

BuildYear_c 0.71278682 0.77146044 14783

Distance_c -1.49753218 -1.28888107 14783

Reform:TradeQ_c -0.56857511 0.91388710 14783

Reform:Size_c -0.06418041 0.05573630 14783

Reform:BuildYear_c -0.21463984 -0.09529907 14783

Reform:Distance_c -0.27456407 0.10141535 147834.3 マッチング法による修正

回帰を行う事前準備としてマッチング法を利用する

重回帰が持つ関数形への依存度を減らせる (Ho et al. 2007)

MathItパッケージを利用

多数のマッチング法が実装されている

4.3.1 Coarsened exact matching

Coarsened exact matching (Iacus, King, and Porro 2012)の実装

- 連続変数をカテゴリー変数化することで、マッチングできるサンプルサイズを増やすことが期待できる

fit.m <- matchit(Reform ~ TradeQ + Size + BuildYear + Distance,

data = Data_R,

method = "CEM"

)- マッチング結果の表示

fit.mA matchit object

- method: Coarsened exact matching

- number of obs.: 14793 (original), 9625 (matched)

- target estimand: ATT

- covariates: TradeQ, Size, BuildYear, DistanceSample sizesにて、マッチングできなかったサンプル数(14793の事例中、9625サンプルがマッチングできなかった)が確認できる

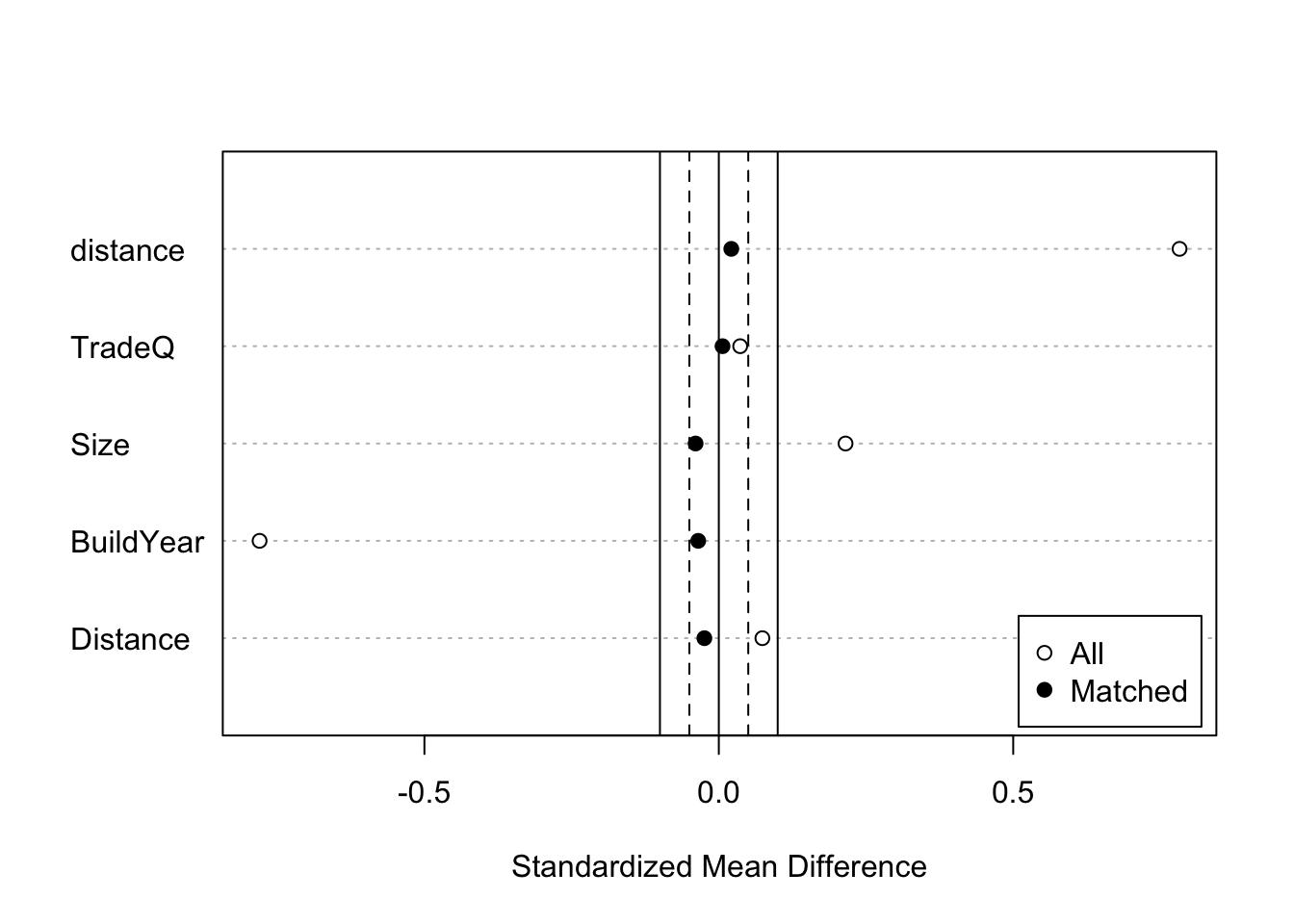

マッチング結果の図示

fit.m |>

summary() |>

plot(abs = FALSE)

- マッチング結果を変数として含んだデータを作成

df <- match.data(fit.m)“subclass”: マッチングしたグループ

“weights”:マッチング後の推計に用いるウェイト

マッチングしたデータを用いた推定

- 新たに作成されるweight (defaltではweights)を用いた、加重推定で実装

lm_robust(Price ~ Reform + TradeQ + Size + BuildYear + Distance,

df,

weights = weights,

clusters = subclass) Estimate Std. Error t value Pr(>|t|) CI Lower

(Intercept) -1311.7224181 49.24745093 -26.635336 1.958605e-69 -1408.8022390

Reform 4.7327819 0.45785352 10.336891 2.940391e-23 3.8336958

TradeQ 0.4481538 0.28287157 1.584301 1.144379e-01 -0.1090656

Size 0.7219818 0.01918252 37.637485 2.430409e-113 0.6842264

BuildYear 0.6615543 0.02458901 26.904467 1.016361e-70 0.6130877

Distance -1.3201228 0.07892931 -16.725382 2.395637e-43 -1.4755318

CI Upper DF

(Intercept) -1214.6425972 211.0880

Reform 5.6318679 636.5110

TradeQ 1.0053732 240.7352

Size 0.7597372 288.6097

BuildYear 0.7100210 214.7855

Distance -1.1647137 264.75444.3.2 Propensity score with subclassification

Coarsened exact matchingでもマッチングできないサンプルが多数出てくる可能性

- とくに\(X\)が大量にある場合

1次元の距離指標を用いて、マッチングを行う

- 距離指標としては、Mahalanobis’ Distance、Propensity scoreなど

ここではPropensity score \(p_d(X)\)を用いる

\[p_d(X)\equiv \Pr[D=d|X]\]

属性\(X\)のユニットの中で、原因変数の値が\(d\)である人の割合

未知の場合、データから推定する必要がある

推定された傾向スコアを用いたStratification マッチング (Imbens 2015 の推奨)

- ロジットにて傾向スコアを推定

fit.m <- matchit(Reform ~ TradeQ + Size + BuildYear + Distance,

data = Data_R,

method = "subclass",

estimand = "ATE"

)- マッチング結果

summary(fit.m)

Call:

matchit(formula = Reform ~ TradeQ + Size + BuildYear + Distance,

data = Data_R, method = "subclass", estimand = "ATE")

Summary of Balance for All Data:

Means Treated Means Control Std. Mean Diff. Var. Ratio eCDF Mean

distance 0.3418 0.2260 0.7825 1.4151 0.2293

TradeQ 2.4827 2.4422 0.0363 1.0239 0.0101

Size 49.8096 45.1755 0.2152 0.7953 0.0438

BuildYear 1993.5456 2003.2632 -0.7800 1.1529 0.1649

Distance 7.2755 6.9736 0.0740 1.0298 0.0149

eCDF Max

distance 0.3455

TradeQ 0.0184

Size 0.1621

BuildYear 0.3415

Distance 0.0337

Summary of Balance Across Subclasses

Means Treated Means Control Std. Mean Diff. Var. Ratio eCDF Mean

distance 0.2576 0.2545 0.0212 1.0285 0.0062

TradeQ 2.4606 2.4535 0.0063 1.0386 0.0060

Size 45.5250 46.3742 -0.0394 0.8215 0.0172

BuildYear 2000.4362 2000.8722 -0.0350 0.9634 0.0093

Distance 6.9579 7.0579 -0.0245 0.9047 0.0061

eCDF Max

distance 0.0160

TradeQ 0.0145

Size 0.0600

BuildYear 0.0353

Distance 0.0151

Sample Sizes:

Control Treated

All 11012. 3781.

Matched (ESS) 10508.41 2553.82

Matched 11012. 3781.

Unmatched 0. 0.

Discarded 0. 0. - マッチング結果の図示

fit.m |>

summary() |>

plot(abs = FALSE)

- マッチングしたデータを用いた推定

lm_robust(Price ~ Reform + TradeQ + Size + BuildYear + Distance,

df,

weights = weights,

clusters = subclass) Estimate Std. Error t value Pr(>|t|) CI Lower

(Intercept) -1311.7224181 49.24745093 -26.635336 1.958605e-69 -1408.8022390

Reform 4.7327819 0.45785352 10.336891 2.940391e-23 3.8336958

TradeQ 0.4481538 0.28287157 1.584301 1.144379e-01 -0.1090656

Size 0.7219818 0.01918252 37.637485 2.430409e-113 0.6842264

BuildYear 0.6615543 0.02458901 26.904467 1.016361e-70 0.6130877

Distance -1.3201228 0.07892931 -16.725382 2.395637e-43 -1.4755318

CI Upper DF

(Intercept) -1214.6425972 211.0880

Reform 5.6318679 636.5110

TradeQ 1.0053732 240.7352

Size 0.7597372 288.6097

BuildYear 0.7100210 214.7855

Distance -1.1647137 264.75444.4 付録:Dot-and-Whisker plotによる可視化

- Dot-and-Whisker図により点推定量と信頼区間を可視化

fit.m <- matchit(Reform ~ TradeQ + Size + BuildYear + Distance,

data = Data_R,

method = "CEM"

)

df <- match.data(fit.m)

Result1 <- lm_robust(Price ~ Reform + TradeQ + Size + BuildYear + Distance,

data = df) |>

tidy() |>

filter(term == "Reform"

) |>

mutate(Method = "OLS")

Result1 |>

ggplot(aes(y = term,

x = estimate,

xmin = conf.low,

xmax = conf.high)

) +

geom_pointrange() +

geom_vline(xintercept = 0) +

theme_bw()

Result2 <- lm_robust(Price ~ Reform + TradeQ + Size + BuildYear + Distance,

data = df,

weights = weights,

clusters = subclass) |>

tidy() |>

filter(term == "Reform"

) |>

mutate(Method = "Matching + OLS")

Result1 |>

bind_rows(Result2) |>

ggplot(aes(y = Method,

x = estimate,

xmin = conf.low,

xmax = conf.high)

) +

geom_pointrange() +

geom_vline(xintercept = 0) +

theme_bw()